Respecting Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements is essential for maintaining security and integrity in the complex world of financial transactions. To prevent financial crimes, maintain openness, and protect the integrity of the global financial system, AML/KYC procedures are essential. We explore the importance, complexities, and changing field of KYC/AML compliance in this piece.

Comprehending AML/KYC

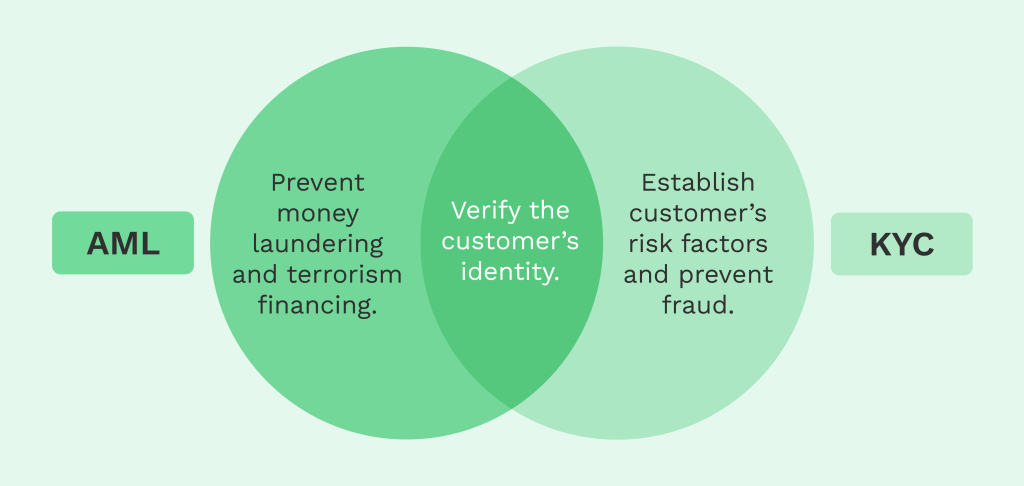

AML is the term for a body of laws, rules, and practices aimed at preventing illicit money from being generated through criminal activity and then incorporated into the legal financial system. Money laundering is a danger to the viability and integrity of financial institutions because it allows criminals to hide the source of money obtained illegally from crimes including drug trafficking, financing of terrorism, corruption, and organized crime.

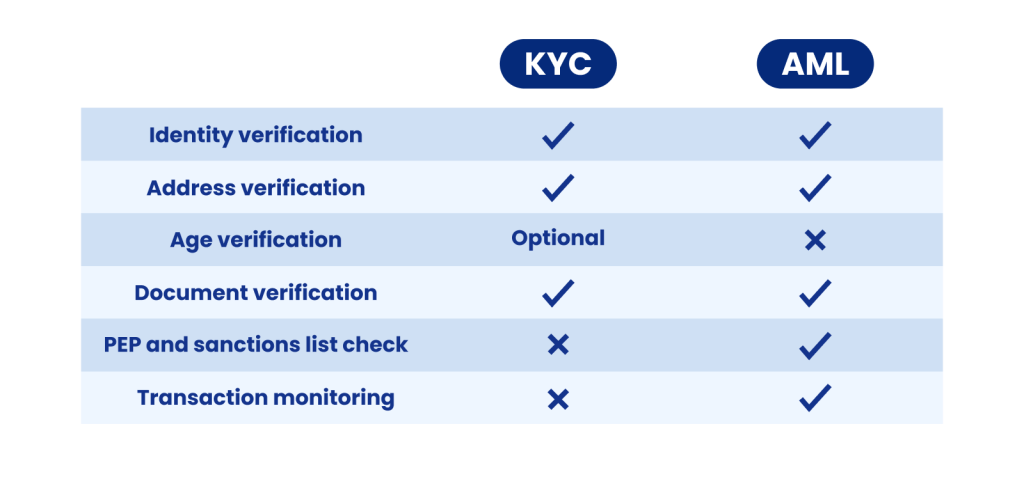

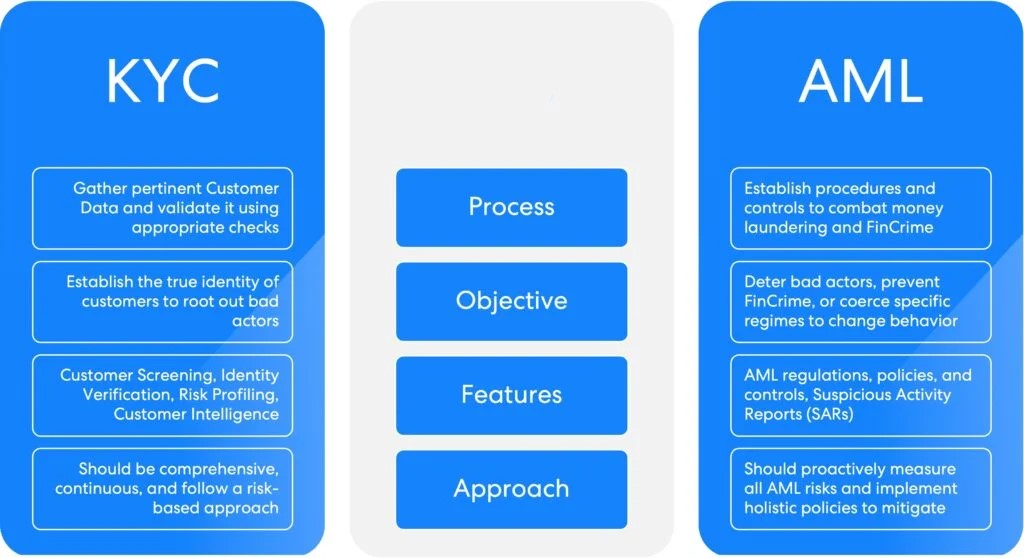

To reduce the possibility of money laundering and other financial crimes, KYC, on the other hand, comprises the process of confirming the identification of clients and evaluating their risk profile. Financial institutions are required by KYC measures to gather pertinent data about their clients, such as transaction history, identity documents, and personal information, to verify the accuracy of their financial transactions and identify any questionable activity.

The Significance of KYC/AML Adherence

One cannot overestimate the significance of KYC/AML compliance because it fulfils several vital functions:

Preventing Financial Crimes

By placing strict due diligence requirements on financial institutions and other regulated businesses, AML/KYC regulations serve as a barrier against money laundering, terrorist funding, fraud, and other illegal financial activities.

Financial Institution Protection

By lowering the possibility of being used for illegal activities and facing legal repercussions, compliance with KYC/AML requirements contributes to the preservation of the stability, integrity, and reputation of financial institutions.

Improving Financial Transparency

By mandating extensive documentation, verification, and reporting of client information and transactional activity, AML/KYC policies encourage accountability and transparency in financial transactions.

Protecting National Security

By stopping the flow of money to terrorist groups and other illicit enterprises that endanger public safety and stability, KYC/AML regulations are essential in protecting national security.

Maintaining Regulatory Compliance

Financial institutions and other designated entities are required to comply with AML/KYC rules, which guarantee adherence to legal obligations and regulatory standards established by national and international authorities.

Explore More Utility Tokens: Exploring the Backbone of Blockchain

Essential Elements of KYC/AML Compliance

A complete framework comprising multiple essential components is necessary for effective AML/KYC compliance.

Customer Due Diligence (CDD)

Financial institutions must perform extensive due diligence on their clients to confirm their identities, evaluate their risk tolerance, and comprehend the scope of their financial activity. This process is known as customer due diligence (or CDD). Enhanced due diligence could be required for transactions involving high-risk customers.

Transaction Monitoring

To identify any odd or suspect activity that would point to possible money laundering or terrorist financing, financial institutions need to put in place systems for tracking customer transactions in real-time.

Suspicious Activity Reporting (SAR)

Financial institutions are required to submit Suspicious Activity Reports (SARs) to the appropriate authorities, such as financial intelligence units or law enforcement agencies, to report any suspicious transactions or activity.

Risk assessment

To identify and assess potential risks related to their clients, goods, services, and locations, financial institutions need to carry out frequent risk assessments. They also need to put in place suitable risk-reduction strategies.

Compliance Education and Awareness

To guarantee that staff members are aware of their responsibilities under KYC/AML laws and are prepared to recognize and report suspicious activity, financial institutions must offer extensive education and awareness programs.

Changing Environment and Difficulties

AML/KYC compliance is a dynamic field that is always changing due to new regulations, technology breakthroughs, and rising threats. To achieve and maintain compliance, financial institutions must overcome several obstacles, including:

Regulation Complexity

The intricate and varied nature of AML/KYC laws, which differ between jurisdictions and are frequently updated and amended, presents difficulties for compliance management.

Technological Innovation

New avenues for money laundering are created by the quick development of technology, including digital banking, cryptocurrencies, and mobile payments. To effectively monitor compliance, new and creative solutions are needed.

Cross-Border Transactions

As a result of globalization, there has been a rise in cross-border transactions, which presents difficulties for financial institutions in terms of keeping an eye on client activity across several jurisdictions and performing due diligence.

Resource Constraints

Smaller financial institutions and non-financial enterprises may find it difficult to meet the requirements of KYC/AML rules due to the significant investments that must be made in technology, human resources, and training.

Emerging dangers

Financial institutions need to be on the lookout for new dangers that could arise, like identity theft, cybercrime, and criminals using new payment methods. These risks call for proactive risk management and mitigation techniques.

In summary

To sum up, AML/KYC compliance is essential to preserving the security, stability, and integrity of the international financial system. Financial institutions and other regulated businesses can help identify and stop money laundering, terrorist funding, and other illegal financial activity by following KYC/AML requirements. Sustaining confidence, transparency, and accountability in financial transactions is contingent upon successful KYC/AML compliance, particularly since the regulatory landscape is always changing and novel difficulties arise.